What is fraud detection and prevention?

Fraud detection and prevention is the process of identifying, stopping, and reducing fraudulent activity before it causes financial, operational, or reputational damage. In 2026, it matters more than ever because fraud is no longer isolated, manual, or slow; it is automated, AI-powered, and embedded across digital systems.

That single definition explains why fraud has moved from a back-office control function to a board-level business risk.

In today’s environment, fraud does not look like a suspicious transaction flagged after the fact. It looks like a normal customer journey, until it isn’t. Synthetic identities pass onboarding. Account takeovers use valid credentials. Deepfake voices authorize real payments. DeFi exploits drain liquidity pools in seconds, not days.

The scale reflects this shift. Businesses lose around 5% of annual revenue to fraud on average, while consumer fraud losses exceeded $12.5 billion in 2024 alone, according to recent regulatory and industry data. In healthcare, governments continue to uncover multi-billion-dollar fraud schemes involving stolen identities and AI-generated documentation. In financial services, account takeover attacks are accelerating faster than most detection teams can adapt. In decentralized finance, fraud is often irreversible by design.

“Fraud is a silent but costly threat that continues to translate into significant financial losses every year.” — Deloitte, Corporate Forensic Services, 2025

The core problem is not that organizations lack fraud tools.

It’s that most fraud prevention strategies were designed for a world where:

Attacks were predictable

Systems were centralized

Fraud happened after a transaction, not during it

That world no longer exists.

Modern fraud operates across legacy systems, cloud platforms, APIs, identity providers, payment rails, and decentralized networks simultaneously. It exploits fragmentation, slow decision-making, and governance gaps more than it exploits technical weaknesses.

As a result, fraud detection and prevention in 2026 is no longer about adding another rule, model, or verification step. It is about whether an organization’s systems, data architecture, and governance model are capable of responding to adaptive, intelligent threats in real time.

This article explains:

What has fundamentally changed in fraud since 2020

How AI-driven fraud detection actually works in practice

Why false positives remain one of the most expensive hidden risks

How healthcare, finance, and DeFi approach fraud differently

Why governance and system design matter as much as machine learning

In short, fraud prevention is no longer a technology problem alone. It is a systems, strategy, and leadership problem, and the organizations that recognize this are the ones that lose less money, detect fraud earlier, and protect trust at scale.

What Has Changed in Fraud Detection Since 2020?

Fraud detection has shifted from rule-based, transaction-level controls to AI-driven, behavior-based systems designed to stop fraud in real time rather than investigate it after losses occur.

Since 2020, three structural changes have reshaped fraud permanently:

Fraud became faster than human review

Attackers adopted AI and automation

Enterprise systems became more fragmented, not less

As a result, traditional fraud prevention models no longer scale.

What fraud detection looked like before 2020

Before 2020, most fraud prevention strategies were built around a predictable model:

Fraud followed known patterns

Attacks reused similar techniques

Detection happened after a transaction

Human analysts reviewed s in batches

Rule-based systems worked because fraud evolved slowly.

If an attack method became common, teams added new rules. If fraud spiked in one channel, controls were tightened there. This approach was imperfect but manageable.

Why that model broke after 2020

Fraud detection stopped working the moment fraud became adaptive.

Three changes accelerated this breakdown:

1. Digital acceleration compressed fraud timelines

E-commerce, digital banking, telemedicine, and DeFi adoption removed friction for customers and criminals. Fraud now happens in seconds, not days.

2. AI lowered the cost of fraud

Criminals began using:

AI-generated identities

Automated credential stuffing

Deepfake audio and video

Scripted transaction testing

Fraud became scalable, not manual.

3. Systems became more complex

Modern enterprises now operate across:

Legacy platforms

Cloud services

Third-party APIs

Payment processors

Identity providers

Decentralized protocols

Each system sees only part of the story.

“AI-generated financial fraud and deepfake identities have made detection and attribution harder, forcing organizations to adopt real-time fraud monitoring.” — Deloitte Romania, 2025

What modern fraud looks like in practice

Modern fraud no longer announces itself.

It blends into legitimate behavior until the moment damage is irreversible.

Examples include:

Synthetic identities that pass onboarding and transact normally for months

Account takeovers using valid credentials and normal devices

Authorized Push Payment (APP) scams where users approve real transfers

DeFi exploits that abuse protocol logic rather than steal credentials

The attack is the journey, not the transaction.

How fraud detection approaches changed as a result

The core shift is simple:

Fraud detection moved from “Is this transaction suspicious?” to “Does this behavior make sense?”

That shift changed everything.

Old vs modern fraud detection models

Dimension | Pre-2020 Fraud Detection | Fraud Detection in 2026 |

Detection logic | Static rules | Adaptive AI models |

Focus | Individual transactions | Behavioral sequences |

Speed | Post-transaction | Real-time / pre-authorization |

Data scope | Single channel | Cross-channel & cross-system |

False positives | High but accepted | Actively minimized |

Human role | Manual review | Oversight & escalation |

What role AI plays — and what it does not

AI did not replace fraud teams. It replaced assumptions.

Modern AI-based fraud detection:

Learns normal behavior continuously

Detects deviations in context, not isolation

Adapts to new fraud patterns without new rules

What it does not do:

Eliminate governance requirements

Remove the need for explainability

Automatically reduce risk without system integration

AI is effective only when embedded into systems that can act on its decisions.

Why false positives became a critical business problem

In older models, false positives were tolerated.

In modern digital environments, they are costly.

High false positive rates lead to:

Abandoned transactions

Locked customer accounts

Increased support costs

Brand trust erosion

Industry data shows that many organizations still experience 60–70% false positive rates, despite advanced tools.

In 2026, false positives are no longer a technical nuisance; they are a revenue and retention problem.

Why governance now matters as much as detection

As fraud became more complex, ownership became less clear.

Common gaps include:

Fraud is owned by compliance, but executed by engineering

Security teams are detecting issues that product teams can’t act on

AI models producing s without clear escalation paths

Modern fraud detection only works when:

Accountability is clearly defined

Decision rights are explicit

Technology, risk, and product teams collaborate

This is why leading organizations treat fraud prevention as a governance discipline, not a toolset.

In short: Fraud detection changed after 2020 because fraud became faster, automated, and behavior-based. Static rules and siloed systems can no longer keep up. Modern fraud prevention relies on AI-driven behavioral analysis, real-time decisioning, and strong governance to stop fraud before losses occur.

Why Traditional Fraud Prevention Systems Fail

Why don’t traditional fraud prevention systems work anymore?

Traditional fraud prevention systems fail because they rely on static rules, fragmented data, and ed decision-making, while modern fraud is adaptive, cross-channel, and happens in real time.

In short, today’s fraud evolves faster than yesterday’s controls.

What “traditional fraud prevention” actually means

Traditional fraud prevention typically includes:

Rule-based engines (if–then logic)

Threshold checks (amounts, frequency, location)

Blacklists and whitelists

Manual reviews after s are triggered

These systems were designed for a world where:

Fraud patterns changed slowly

Channels were limited

Human review could keep up with volume

That context no longer exists.

The five core reasons traditional systems break down

1. Static rules cannot adapt to adaptive fraud

Rule-based systems only detect what they are explicitly told to look for.

Modern fraud:

Changes tactics rapidly

Tests controls automatically

Avoids known thresholds by design

Once a rule becomes effective, attackers simply route around it.

Result: constant rule inflation, declining accuracy, and growing maintenance cost.

2. Fragmented data hides the fraud story

Most legacy systems analyze fraud in silos:

Payments see transactions

Identity systems see logins

CRM sees customers

Support sees complaints

No single system sees behavior across the entire journey.

Fraud, however, operates across all of them.

Result: each system sees “normal,” while the combined pattern is clearly fraudulent.

3. Detection happens too late

Traditional fraud systems often detect fraud:

After authorization

After settlement

After customer complaints

At that point:

Money is already gone

Chargebacks are unavoidable

Trust is already damaged

In high-velocity environments like fintech and DeFi, late detection is equivalent to no detection at all.

4. False positives overwhelm real risk

Legacy systems generate s by being conservative.

This leads to:

False positive rates of 60–70%

Analyst fatigue

Slower response to real fraud

Poor customer experience

The paradox:

The more rules you add, the less effective detection becomes.

5. Governance is unclear or missing

In many organizations:

Compliance owns fraud policy

Security owns detection

Product owns user experience

Engineering owns systems

When fraud spans all four, no one owns the outcome.

This results in:

s without action

Conflicting priorities

Slow escalation

Inconsistent decisions

Fraud prevention fails not because teams are incapable, but because ownership is fragmented.

Is rule-based fraud detection still useful?

Yes, but only as a supporting layer. Rule-based controls are effective for known patterns and regulatory requirements, but they are insufficient on their own against adaptive, AI-driven fraud.

Old assumptions vs modern reality

Assumption | Why It No Longer Holds |

Fraud repeats patterns | Fraud mutates constantly |

One system can detect fraud | Fraud spans multiple systems |

Manual review can scale | Volume exceeds human capacity |

More rules = better security | More rules = more noise |

Detection is enough | Prevention must happen earlier |

Why adding more tools doesn’t fix the problem

A common response to rising fraud is to add:

Another verification step

Another fraud vendor

Another review workflow

This often increases friction without reducing losses.

Why?

Because tools added to broken architectures inherit the same limitations:

Siloed data

ed action

Unclear accountability

Fraud prevention is constrained by system design, not tool count.

What modern fraud prevention requires instead

Effective fraud prevention in 2026 requires:

Cross-system data visibility

Real-time behavioral analysis

Adaptive risk scoring

Clear decision ownership

Governance aligned with technology

This is a systems problem, not a feature gap.

In short, traditional fraud prevention systems fail because they rely on static rules, siloed data, and late detection. Modern fraud is adaptive, cross-channel, and behavior-driven, requiring real-time analysis, integrated systems, and clear governance to stop losses before they occur.

How AI-Driven Fraud Detection Actually Works in 2026

How does AI improve fraud detection in 2026?

AI improves fraud detection by analyzing behavior, context, and relationships in real time, allowing organizations to detect fraud before transactions are completed, not after losses occur.

Unlike traditional systems that evaluate isolated events, AI-driven fraud detection evaluates patterns over time, across users, devices, sessions, and systems.

What AI-driven fraud detection really means

AI-driven fraud detection is often misunderstood as “using machine learning instead of rules.”

In practice, it means something more specific:

Decisions are based on probability, not binary rules

Risk is evaluated continuously, not at fixed checkpoints

Signals are combined across multiple systems, not one channel

AI does not replace fraud logic.

It redefines how risk is calculated and acted upon.

Core components of AI-driven fraud detection

AI-based fraud prevention systems rely on four foundational layers.

1. Behavioral analytics (the foundation layer)

Behavioral fraud detection analyzes how users interact with systems, not just what actions they perform.

Instead of asking:

“Is this transaction suspicious?”

The system asks:

“Does this behavior make sense for this user right now?”

Behavioral signals include:

Navigation patterns

Interaction speed and rhythm

Session flow and sequencing

Device and environment consistency

Because behavior is difficult to fake consistently, it is one of the strongest fraud indicators available.

What is behavioral fraud detection?

Behavioral fraud detection identifies fraud by monitoring deviations from normal user behavior, such as unusual navigation patterns, interaction speed, or session sequences, rather than relying solely on transaction details.

2. Machine learning models (risk estimation layer)

Machine learning models estimate the likelihood that an action is fraudulent based on historical and real-time data.

In mature systems, multiple models operate together.

Common model types:

Model Type | What It’s Used For | Key Limitation |

Supervised ML | Known fraud patterns | Needs labeled data |

Unsupervised ML | Unknown anomalies | Requires tuning |

Semi-supervised ML | Hybrid detection | Higher complexity |

Deep learning | High-dimensional data | Explainability challenges |

No single model is sufficient.

Accuracy comes from orchestration, not model choice.

3. Graph and network analysis (relationship layer)

Graph-based fraud detection focuses on relationships rather than individuals.

This is critical for detecting:

Synthetic identity rings

Mule networks

Coordinated attacks

DeFi wallet clusters

Instead of evaluating one account, graph models analyze:

Shared devices

Shared credentials

Shared transaction paths

Repeated behavioral links

This approach is particularly effective in financial services and DeFi, where fraud rarely occurs in isolation.

Why is graph analysis important for fraud detection?

Graph analysis helps detect fraud networks by identifying hidden relationships between accounts, devices, or wallets that may appear legitimate when viewed individually.

4. Real-time decision orchestration

Detection without action does not prevent fraud.

Modern AI-driven systems must:

Score risk in milliseconds

Trigger decisions before authorization

Apply proportional responses

Examples of real-time actions:

Step-up authentication

Transaction or rejection

Session termination

Human review escalation

This orchestration layer is where many organizations fail — not because AI is weak, but because systems cannot act fast enough.

Why AI reduces false positives

High false positives are not caused by “bad AI.” They are caused by insufficient context.

AI reduces false positives by:

Evaluating behavior over time, not one event

Weighing multiple weak signals instead of one strong rule

Adjusting thresholds dynamically based on risk

When properly integrated, AI systems:

Block fewer legitimate users

Escalate fewer low-risk cases

Allow fraud teams to focus on real threats

What AI cannot do on its own

AI-driven fraud detection has limits.

AI cannot:

Fix fragmented data architectures

Replace governance and ownership

Guarantee regulatory compliance without explainability

Compensate for ed system responses

This is why AI effectiveness depends on system design and integration, not just model quality.

AI in regulated and decentralized environments

Different industries apply AI differently:

Healthcare: privacy-preserving and explainable models

Financial services: real-time scoring with auditability

DeFi: on-chain analytics and automated response logic

In all cases, AI must operate within clear governance boundaries to remain effective and compliant.

In short: AI-driven fraud detection works by analyzing behavior, relationships, and context in real time. It replaces static rules with adaptive risk scoring, reduces false positives, and enables earlier intervention, but only when integrated into systems that can act on its decisions.

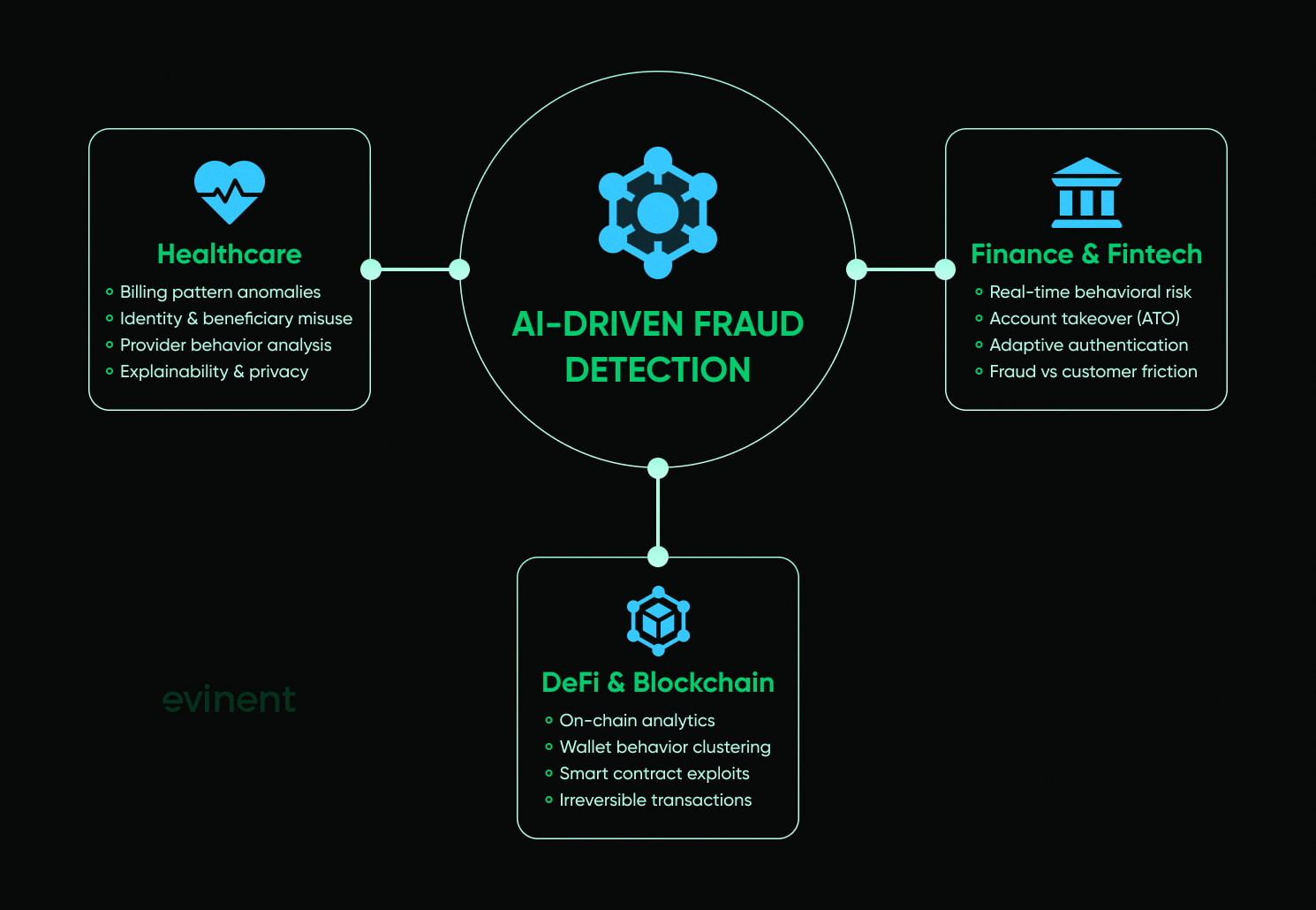

Fraud Detection by Industry — Healthcare, Finance, and DeFi

How does fraud detection differ by industry?

Fraud detection differs by industry because fraud exploits the weakest points in each sector’s systems, incentives, and regulatory constraints.

Healthcare fraud targets billing and identity gaps. Financial fraud exploits speed and trust. DeFi fraud abuses protocol logic and irreversibility.

While the underlying principles of AI-driven fraud detection are consistent, implementation and priorities vary significantly by sector.

Fraud Detection in Healthcare

How is fraud detected in healthcare systems?

Healthcare fraud detection focuses on identifying abnormal billing patterns, identity misuse, and documentation inconsistencies across highly regulated, data-sensitive systems.

Healthcare fraud is often low-visibility but high-impact, accumulating over time rather than triggering immediate alarms.

Common healthcare fraud schemes in 2026

Duplicate or inflated billing

Phantom procedures

Identity theft and beneficiary misuse

AI-generated medical documentation

Provider–patient collusion

Unlike payment fraud, these schemes often:

Appear operationally “normal”

Involve legitimate providers

Exploit fragmented legacy systems

How AI improves healthcare fraud detection

AI is particularly effective in healthcare because of pattern density.

Key techniques include:

Claims anomaly detection across providers

Behavioral profiling of billing practices

Temporal analysis of treatment sequences

Identity correlation across claims and records

Healthcare authorities now use AI to block fraudulent claims before payment, not merely investigate after losses.

Why is healthcare fraud hard to detect?

Healthcare fraud is difficult to detect because it often involves legitimate providers, complex billing rules, and ed visibility into abnormal patterns across multiple systems.

Key constraint: privacy and explainability

Healthcare fraud detection must balance:

Effectiveness

Patient privacy

Regulatory compliance

This makes explainable AI and secure system architecture mandatory, not optional.

In short:

Healthcare fraud detection relies on AI-driven pattern analysis across claims, identities, and providers, with a strong emphasis on explainability, privacy, and system integration.

Fraud Detection in Financial Services and Fintech

How do banks and fintechs detect fraud in 2026?

Financial institutions detect fraud using real-time behavioral analysis, transaction risk scoring, and adaptive authentication to stop fraud before funds move.

Speed is both the opportunity and the risk.

Dominant fraud types in finance

Account takeover (ATO)

Authorized Push Payment (APP) scams

Payment fraud and chargeback abuse

Credential stuffing

Insider-enabled fraud

Many attacks use valid credentials, making traditional controls ineffective.

What modern financial fraud detection focuses on?

Rather than blocking transactions outright, modern systems:

Continuously score session risk

Adjust authentication dynamically

Combine behavior, device, and transaction data

Minimize friction for low-risk users

This approach allows institutions to:

Reduce false positives

Protect customer experience

Meet regulatory expectations

Why do valid credentials still lead to fraud?

Because credentials can be stolen, reused, or socially engineered, modern fraud detection focuses on behavior and context rather than credentials alone.

Key challenge: customer trust vs security

Overly aggressive controls lead to:

Abandoned transactions

Customer churn

Support overload

Effective fraud detection balances security and usability, not one at the expense of the other.

In short: Financial fraud detection prioritizes real-time behavioral risk scoring and adaptive responses to stop account takeovers and payment fraud without harming legitimate users.

Fraud Detection in DeFi and Blockchain Systems

How is fraud detected in DeFi?

DeFi fraud detection relies on on-chain analytics, graph models, and protocol-level monitoring because transactions are irreversible and attackers are pseudonymous.

There is no central authority to reverse mistakes — prevention is the only defense.

Common DeFi fraud vectors

Smart contract exploits

Governance attacks

Liquidity pool manipulation

Rug pulls and exit scams

Flash loan abuse

These attacks exploit logic, not users.

How AI and analytics are applied in DeFi

DeFi fraud detection focuses on:

Transaction graph analysis

Wallet behavior clustering

Abnormal contract interaction patterns

Real-time anomaly detection

Because everything is public, data availability is high, but action windows are extremely small.

Why is fraud prevention harder in DeFi?

Fraud prevention is harder in DeFi because transactions are irreversible, attackers are anonymous, and exploits can execute automatically at machine speed.

Key limitation: enforcement

Even when fraud is detected:

Funds may already be gone

Mitigation depends on protocol design

Governance response may be slow

This makes secure system architecture and monitoring at design stage critical.

In short: DeFi fraud detection depends on real-time on-chain analytics and protocol-level safeguards, because post-transaction recovery is often impossible.

Cross-Industry Insight

Despite differences, one conclusion holds across all sectors:

Fraud detection succeeds or fails based on system design, data integration, and governance — not industry alone.

Organizations that modernize fragmented systems and embed fraud prevention into architecture consistently:

Detect fraud earlier

Lose less money

Reduce false positives

Protect trust

In short:

Healthcare focuses on billing and identity patterns, finance prioritizes real-time behavioral risk, and DeFi relies on on-chain analytics. Different threats — same requirement: integrated, AI-driven systems with clear governance.

Fraud Governance, Oversight, and Organizational Accountability

What is fraud governance, and why does it matter in 2026?

Fraud governance is the framework that defines who owns fraud risk, how decisions are made, how incidents are escalated, and how accountability is enforced across the organization.

In 2026, it matters because even the best fraud detection technology fails without clear ownership and decision authority.

Fraud resilience does not start with algorithms.

It starts with leadership.

Why fraud became a governance problem — not just a technical one

As fraud grew more sophisticated, it stopped fitting neatly into one function.

Today:

Fraud involves risk, security, product, engineering, legal, and customer experience

Decisions must be made in real time

Trade-offs between security and usability are unavoidable

When governance is unclear, organizations experience:

s without action

Conflicting priorities

ed responses

Inconsistent customer outcomes

Technology detects risk. Governance decides what happens next.

How poor governance undermines fraud prevention

Even organizations with advanced AI tools struggle when:

Fraud ownership is split across teams

Escalation paths are undefined

Decision rights are unclear

KPIs reward growth over risk control

In these environments, fraud prevention becomes reactive and fragmented — regardless of tooling.

Who should own fraud prevention in an enterprise?

Fraud prevention should be owned at executive level, typically under a Chief Risk, Compliance, or Security leader, with clear cross-functional authority and board oversight.

What effective fraud governance looks like

High-performing organizations treat fraud as a strategic risk domain, not an operational nuisance.

Key characteristics include:

Board-level visibility into fraud exposure and trends

Executive ownership with authority to act across teams

Clear escalation models for high-risk events

Defined decision thresholds for automated vs human action

Governance aligns detection, response, and accountability into a single operating model.

The role of leadership and “tone from the top”

Leadership sets the boundaries within which fraud prevention operates.

When executives:

Prioritize short-term growth over controls

Penalize friction without context

Treat fraud losses as “cost of doing business”

Fraud risk compounds silently.

In contrast, organizations with strong fraud cultures:

Encourage early escalation

Invest in system resilience

Accept short-term friction to prevent long-term loss

Fraud resilience is a leadership decision.

Governance operating model

A mature fraud governance model typically includes:

Layer | Responsibility |

Board | Risk appetite, oversight |

Executive leadership | Ownership, prioritization |

Fraud & risk teams | Detection strategy |

Engineering & product | System implementation |

Operations | Incident response |

Legal & compliance | Regulatory alignment |

No single team can succeed in isolation.

Why governance maturity correlates with lower fraud losses

Industry research consistently shows that organizations with:

Clear governance structures

Defined escalation paths

Integrated systems

Detect fraud earlier and lose significantly less money than peers with fragmented oversight.

Early detection is not luck — it is governance in action.

Governance challenges unique to AI-driven fraud detection

AI introduces new governance requirements:

Model explainability

Bias monitoring

Auditability

Accountability for automated decisions

Without governance:

AI decisions become opaque

Regulatory exposure increases

Trust erodes internally and externally

AI does not remove responsibility — it raises the bar for it.

In short, fraud governance defines ownership, decision-making, and accountability for fraud risk. In 2026, strong governance is as critical as AI technology because detection without clear authority and escalation fails to prevent losses.

How to Build a Modern Fraud Prevention Architecture

What is a modern fraud prevention architecture?

A modern fraud prevention architecture is a system-level design that integrates identity intelligence, behavioral analytics, AI decisioning, and governance controls to prevent fraud in real time across all channels.

Unlike traditional setups that bolt fraud checks onto isolated systems, modern architectures are designed for fraud by default.

Why architecture matters more than tools

Many organizations invest in advanced fraud tools and still struggle.

The reason is structural.

Fraud prevention fails when:

Data is fragmented across systems

Decisions are ed by architecture

AI insights cannot trigger action

Ownership is unclear at runtime

Architecture determines whether fraud detection can actually prevent fraud.

Core principles of modern fraud prevention architecture

Before looking at components, mature organizations align on four principles:

Real-time by design

Fraud decisions must happen before authorization, not after settlement.

Behavior-first, not transaction-first

Systems must evaluate sequences of actions, not isolated events.

Cross-system visibility

Identity, payments, devices, and sessions must be correlated.

Governance-aware automation

Automated decisions must align with risk appetite and escalation rules.

The five-layer fraud prevention architecture model

Most effective enterprise architectures follow a layered approach.

1. Identity and device intelligence layer

Purpose: establish who (or what) is interacting with the system.

This layer aggregates:

Identity attributes

Device fingerprints

Network and environment signals

Historical risk context

It provides baseline trust scoring — not final decisions.

2. Behavioral analytics layer

Purpose: detect intent through behavior.

This layer analyzes:

Session flow

Interaction timing

Navigation patterns

Inconsistencies over time

Behavioral analytics is critical because credentials and devices can be stolen — behavior is harder to fake consistently.

3. Risk scoring and AI decision layer

Purpose: translate signals into probabilistic risk.

This layer:

Combines identity, behavior, and transaction data

Applies multiple AI models

Produces dynamic risk scores

Adjusts thresholds in real time

Risk scoring must be continuous, not checkpoint-based.

4. Decision orchestration and response layer

Purpose: act on risk immediately and proportionally.

Possible responses include:

Step-up authentication

Transaction s or limits

Session termination

Escalation to human review

This layer is where many architectures fail — not because AI is weak, but because systems cannot respond fast enough.

5. Governance, audit, and feedback layer

Purpose: ensure accountability, learning, and compliance.

This layer supports:

Explainability and audit trails

Model performance monitoring

Bias and drift detection

Continuous improvement loops

Without this layer, fraud prevention becomes opaque and unsustainable.

What is the most important layer in fraud prevention architecture?

There is no single most important layer. Fraud prevention only works when identity, behavior, AI decisioning, response mechanisms, and governance operate together as one system.

Why legacy architectures struggle to support this model

Legacy systems typically:

Store data in silos

Operate in batch mode

Depend on manual escalation

Cannot support real-time orchestration

As a result:

AI insights arrive too late

Fraud decisions are ed

Losses occur despite detection

This is why modern fraud prevention often requires system modernization, not just tool adoption.

Build vs integrate: a strategic decision

Organizations face two paths:

Incremental integration into existing systems

Architectural modernization to support fraud natively

Incremental approaches work short-term. Modernized architectures win long-term.

The right choice depends on:

Fraud exposure

System complexity

Regulatory environment

Growth trajectory

In short: A modern fraud prevention architecture integrates identity intelligence, behavioral analytics, AI risk scoring, real-time response, and governance into a single system. Architecture — not tools alone — determines whether fraud detection can actually prevent losses.

Measuring Fraud Prevention ROI: What Executives Should Track

How do executives measure the ROI of fraud detection and prevention?

Executives measure fraud prevention ROI by tracking how effectively the organization reduces losses, detects fraud earlier, minimizes false positives, and protects customer trust, not by counting how many fraud s are generated.

In 2026, ROI is about business impact, not technical activity.

Why traditional fraud metrics mislead leadership

Many organizations still report:

Number of s generated

Rules triggered

Cases reviewed

These metrics say nothing about:

Money saved

Customers retained

Risk avoided

Trust preserved

Fraud prevention ROI must be measured in outcomes, not effort.

The four ROI dimensions that matter

Effective fraud leaders evaluate ROI across four interconnected dimensions.

1. Fraud loss reduction

What it measures: How much financial loss is prevented or avoided over time.

Key indicators:

Net fraud losses (absolute and percentage of revenue)

Losses prevented before authorization

Reduction in repeat fraud

Why it matters:

Direct impact on profitability

Clear signal of prevention effectiveness

2. Detection speed and intervention timing

What it measures: How early fraud is detected in the attack lifecycle.

Key indicators:

Time to detection

Percentage of fraud stopped pre-authorization

Time from anomaly to action

Earlier detection consistently correlates with:

Lower financial losses

Fewer chargebacks

Reduced regulatory exposure

3. False positives and customer friction

What it measures: How often legitimate customers are incorrectly flagged or blocked.

Key indicators:

False positive rate

Customer complaints related to fraud controls

Abandoned transactions due to friction

Support tickets triggered by fraud checks

High false positives are not “acceptable trade-offs” — they are hidden revenue leaks.

4. Operational efficiency and scalability

What it measures:

How effectively fraud teams operate as volume increases.

Key indicators:

s per analyst

Automation rate

Manual review reduction

Cost per case

AI-driven systems should reduce manual workload without increasing risk.

Executive KPI snapshot

KPI | Why It Matters to Leadership |

Net fraud loss | Direct financial impact |

Fraud loss as % of revenue | Risk normalization |

False positive rate | Customer experience |

Time to detection | Prevention effectiveness |

Cost per fraud case | Operational efficiency |

Repeat fraud rate | Control durability |

What is a good fraud detection ROI benchmark?

A strong fraud prevention program shows declining fraud losses, faster detection times, and decreasing false positive rates as transaction volume grows — not flat or rising costs.

Why ROI improves only after architecture and governance changes

Organizations often invest heavily in fraud tools but see limited ROI.

The reason is structural.

ROI improves only when:

Systems can act in real time

AI insights trigger decisions

Governance aligns incentives

Data flows across platforms

Without these foundations, detection improves — but prevention does not.

Connecting fraud ROI to broader business outcomes

Mature organizations link fraud metrics to:

Customer lifetime value

Conversion rates

Churn

Brand trust

Regulatory performance

Fraud prevention becomes a growth enabler, not just a loss control.

In short: Fraud prevention ROI is measured by loss reduction, detection speed, false positive reduction, and operational efficiency. Executives should focus on outcomes that protect revenue, customers, and trust — not volume.

Fraud Trends to Watch in 2026–2027: What Leaders Should Prepare For

What fraud trends will shape the next two years?

Between 2026 and 2027, fraud will become more automated, more personalized, and more difficult to distinguish from legitimate activity, driven primarily by AI, system complexity, and regulatory pressure.

The most important shift is this: Fraud is no longer just evolving; it is co-evolving with detection systems.

1. AI-vs-AI fraud escalation

What’s changing:

Attackers now use AI not only to execute fraud, but to probe, learn, and adapt to fraud detection systems.

Examples include:

Automated testing of transaction thresholds

AI-generated behavior that mimics legitimate users

Rapid mutation of attack patterns once controls are detected

This creates an arms race where:

Static models degrade quickly

Continuous learning becomes mandatory

Model governance becomes as important as model accuracy

Implication for leaders:

Fraud prevention must be treated as a living system, not a deployed solution.

2. Deepfake-enabled social engineering at scale

What’s changing:

Deepfake audio and video are no longer rare or expensive. They are becoming accessible and convincing enough to bypass traditional verification processes.

Emerging risks include:

Executive impersonation for payment authorization

Fake customer support interactions

Synthetic “trusted voices” in internal workflows

These attacks target human trust, not system vulnerabilities.

Implication for leaders:

Fraud controls must extend beyond technical checks to include process design and verification workflows.

3. Synthetic identity fraud dominance

What’s changing:

Synthetic identity fraud is increasingly becoming the default form of identity fraud, not an edge case.

Key characteristics:

Blends real and fake data

Passes onboarding checks

Behaves “normally” for extended periods

Produces losses over time, not instantly

Because these identities mature before monetization, detection requires longitudinal behavioral analysis, not point-in-time checks.

Implication for leaders:

Short-term metrics will miss long-term fraud exposure unless behavior is tracked across lifecycle stages.

4. Fraud shifting earlier in the customer journey

What’s changing:

Fraud is moving upstream — from transactions to onboarding, engagement, and account changes.

Targets include:

Account creation

Credential recovery

Payment method updates

Privilege escalation events

Organizations focused only on transaction monitoring will consistently detect fraud too late.

Implication for leaders:

Fraud prevention must be embedded across the entire customer lifecycle, not just payments.

5. Increased regulatory scrutiny of AI-driven decisions

What’s changing:

As AI becomes central to fraud prevention, regulators are paying closer attention to:

Explainability

Bias and fairness

Decision accountability

Auditability

This applies especially to:

Financial services

Healthcare

Cross-border platforms

AI that cannot explain or justify decisions creates regulatory and reputational risk, even if it performs well technically.

Implication for leaders:

Fraud prevention strategies must balance effectiveness with transparency and governance.

6. Architecture and modernization are becoming risk factors

What’s changing:

Legacy and fragmented architectures are increasingly recognized as risk amplifiers, not neutral infrastructure.

Organizations with:

Batch processing

Siloed data

Manual escalation paths

Will struggle to:

Act in real time

Apply AI decisions consistently

Scale without rising losses

Implication for leaders:

Fraud resilience will increasingly depend on system modernization, not incremental controls.

Will fraud losses continue to grow despite better technology?

Yes, unless organizations modernize systems and governance. Fraud losses grow when detection improves but prevention cannot act fast enough.

What leaders should do now

To prepare for 2026–2027, executives should focus on:

Architecture readiness for real-time decisions

Governance frameworks for AI-driven controls

Cross-functional ownership of fraud risk

Long-term behavioral monitoring capabilities

Fraud prevention is no longer a defensive function — it is a strategic resilience capability.

In short: Future fraud will be AI-driven, behavior-based, and increasingly human-targeted. Organizations that fail to modernize systems, governance, and architecture will detect fraud, but too late to prevent losses.

Final Takeaways for Executives: How to Build Fraud-Resilient Organizations

What should executives take away from modern fraud detection and prevention?

Fraud resilience in 2026 is not achieved by deploying better tools. It is achieved by building systems, governance, and architectures that can adapt faster than fraud itself.

This is the defining shift.

The five truths leaders must internalize

Fraud is now a systemic risk, not an operational issue

Fraud impacts revenue, customer trust, regulatory exposure, and brand equity. Treating it as a back-office function guarantees ed responses and avoidable losses

Detection without prevention is failure

Identifying fraud after funds move or trust is broken is no longer sufficient. Value is created only when systems can act before damage occurs

AI is necessary — but not sufficient

Machine learning improves detection accuracy, but without real-time orchestration, integrated data, and governance, AI insights arrive too late to matter

False positives are a business liability

Every unnecessary block, challenge, or account lock erodes customer trust and revenue. Reducing fraud losses while increasing friction is not a success. Organizations with fragmented systems and unclear ownership consistently lose more to fraud, regardless of tooling.

What fraud-resilient organizations do differently

Fraud-resilient enterprises share a common operating model:

Fraud risk is owned at executive level

Governance defines decision rights and escalation paths

Systems are designed for real-time, cross-channel visibility

AI decisions are explainable, auditable, and accountable

Fraud prevention is embedded across the entire customer lifecycle

They modernize systems not to “fight fraud,” but to remove the conditions that fraud exploits.

Is fraud prevention a technology problem or a leadership problem?

Fraud prevention is both, but leadership determines whether technology can succeed. Without governance, ownership, and architectural readiness, even advanced AI systems fail to prevent losses.

The strategic reframing that matters most

The most important mindset shift for executives is this:

Fraud prevention is not about stopping criminals. It is about designing organizations that remain resilient under constant attack.

In an environment where fraud is automated, adaptive, and persistent, resilience — not perfection — is the goal.

In short:

Fraud-resilient organizations combine AI-driven detection, real-time system architecture, and strong governance. Executives who treat fraud as a strategic systems problem — not a tooling gap — detect fraud earlier, lose less money, and protect trust at scale.

How Evinent Supports Fraud Detection and Prevention Initiatives

Evinent helps enterprises strengthen fraud detection and prevention by modernizing the systems and architectures that fraud exploits most often.

Rather than positioning fraud as a standalone tool problem, Evinent approaches it as a systems, data, and governance challenge.

Across industries such as financial services, healthcare, and digital platforms, Evinent supports organizations by:

Modernizing legacy systems that prevent real-time fraud decisions

Integrating fragmented data sources into unified, behavior-aware architectures

Enabling AI-driven risk analysis within regulated, auditable environments

Designing scalable platforms that support fraud prevention across the full customer lifecycle

Evinent’s work typically focuses on infrastructure readiness, system integration, and architectural resilience, ensuring that AI-driven fraud detection can operate effectively — not just exist as an isolated capability.

For executive teams, this means:

Faster detection-to-action cycles

Lower false positives due to better context

Clearer ownership and governance alignment

Fraud prevention that scales with growth, not against it

Ready to Assess Your Fraud Resilience?

If your organization is detecting fraud but still absorbing losses, the issue may not be your tools — it may be your systems, architecture, or governance model.

Evinent works with enterprise teams to assess fraud readiness, modernize fragmented systems, and enable real-time, AI-driven fraud prevention that aligns with regulatory and business realities.

Start with a focused fraud resilience assessment to understand:

Where detection breaks down before action

Which architectural gaps increase fraud exposure

How governance impacts fraud response speed and accuracy

Share